House hunting is exciting. It is also where many buyers start making emotional decisions before the finance is clear. In a market where prime lending is around 10.5%, bond pre-approval is not a nice-to-have. It is one of the smartest steps you can take before you book viewings or sign an offer to purchase.

Pre-approval gives you an informed view of what you may qualify for based on your income, expenses and credit profile. It does not guarantee final approval, because the bank must still assess the property and final documents, but it helps you start from a stronger position.

What is bond pre-approval?

Bond pre-approval is an assessment of your borrowing potential before you commit to a specific property. It usually looks at your income, expenses, existing debts and credit behaviour. The aim is to estimate a price range that is realistic for your household.

It is different from a final bond grant. Final approval happens after you have signed an offer to purchase and the bank has assessed the property, the purchase price and all supporting documents. Pre-approval is the preparation stage; final approval is the formal decision.

Why it matters more when rates are higher

When interest rates are lower, some buyers have more room in the budget. When rates increase, that room shrinks. A buyer who could afford a certain purchase price a few months ago may need to adjust expectations after the latest increase.

Pre-approval helps you avoid shopping with outdated numbers. It also lets you see the repayment at the current rate, so you can decide whether the price bracket still feels comfortable.

For the official interest rate context, see the SARB Monetary Policy Committee statement.

It protects you from overcommitting

Many buyers calculate affordability by looking at the bond repayment only. That is not enough. A home comes with rates and taxes, levies, insurance, maintenance, electricity, water, security and moving costs. Pre-approval encourages a more realistic budget before you take on the commitment.

Overcommitting is stressful because property is not easy to reverse. Selling quickly can be expensive and uncertain. It is far better to choose a home you can enjoy comfortably than a home that looks impressive but leaves no room for normal life.

It makes your offer stronger

Sellers and estate agents want to know whether a buyer can get finance. A pre-approved buyer is often taken more seriously because they have already started the finance process. This can help when there are competing offers or when you need the seller to consider a reasonable price negotiation.

Pre-approval also helps you act faster. Good properties can move quickly. When your affordability is already checked and your documents are ready, you can make decisions with more confidence.

It helps you negotiate with your eyes open

Knowing your upper limit does not mean you should offer your upper limit. It means you can negotiate strategically. If you are pre-approved up to a certain amount, you can still offer less based on the property condition, comparable sales and your comfort level.

A clear budget also makes it easier to walk away from a deal that does not make sense. That discipline is especially important when buyers feel pressure from agents, family or the fear of missing out.

Here is a simple example of how a 0.25% increase can affect a 20-year bond, before fees, insurance and other property costs:

| Bond amount | At 10.25% | At 10.50% | Approx. difference |

| R1 000 000 | R9 816 | R9 984 | R167 p/m |

| R1 500 000 | R14 725 | R14 976 | R251 p/m |

| R2 000 000 | R19 633 | R19 968 | R335 p/m |

| R2 500 000 | R24 541 | R24 959 | R418 p/m |

This is an estimate only. Your final instalment depends on your approved rate, term, deposit, insurance, fees and bank conditions.

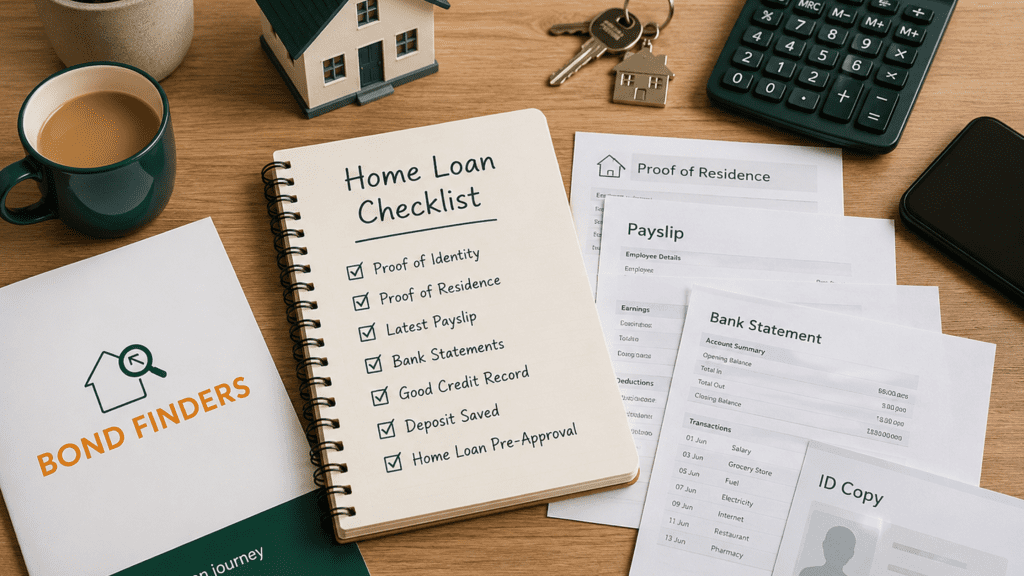

What documents do you need for pre-approval?

For salaried buyers, the usual documents include your ID, proof of address, latest payslip, bank statements and details of income and expenses. For self-employed buyers, banks often need more detail, including financial statements, tax information and business bank statements.

The cleaner and more complete your documents are, the smoother the process usually is. Bank statements should clearly show income and regular commitments. Avoid unexplained transfers where possible, and be ready to explain once-off payments.

What pre-approval does not do

Pre-approval does not lock in the final interest rate forever. It does not guarantee that every property in your price range will be accepted by the bank. It also does not mean you should spend the maximum amount available. Treat it as a guide and a planning tool.

Final approval still depends on the signed offer, bank valuation, property type, legal checks and your financial position at the time of formal application.

How Bond Finders makes pre-approval easier

Bond Finders helps buyers understand what they can afford, prepare the right documents and approach the home loan process with a clear plan. We work with leading banks and help compare options, so you are not relying on one answer from one lender.

Our role is to make the process simpler, clearer and less stressful. Whether you are a first-time buyer, upgrading, relocating or investing, pre-approval helps you start from a position of confidence.

Quick questions buyers are asking

Is pre-approval free? Bond Finders can guide you through the process at no cost to you.

Does pre-approval affect my credit score? A formal credit check can leave a record, depending on the process used. The benefit is that you get a clearer view before applying for a full bond.

How soon should I get pre-approved? Ideally before you start serious house hunting, especially if you plan to make an offer within the next few weeks.

| Ready to move with confidence? Let Bond Finders help you compare bank offers and understand your numbers before you commit. Apply through Bond Finders |

Need personal guidance? Speak to the Bond Finders team before making your next property move.